Segregation of duties necessary for nonprofit organizations

Dec. 30, 2019

This paid piece is sponsored by Eide Bailly LLP.

Would you be comfortable sleeping with all your doors unlocked and your garage door open? Segregation of duties within your nonprofit organization should be treated with the same level of caution and awareness as locking your doors for security.

What is “segregation of duties?”

In simple terms, segregation of duties involves having more than one person required to complete a task or process. That means no one individual should be responsible for initiating, approving and recording transactions. By allowing one person to handle all the financial and accounting duties, your organization is creating an opportunity for fraud that may prove too tempting to resist. The three components that lead to a higher risk for fraud include pressure, rationalization and opportunity. Through proper segregation of duties, you can eliminate the opportunity, reducing the risk of fraud.

For many nonprofit organizations, there aren’t enough individuals in the accounting department to achieve full segregation of duties. Therefore, each nonprofit needs to become creative when structuring its processes to incorporate the individual at the front desk, an executive director or even an individual from governance.

The mission of the organization may sing to your heart strings, but sometimes the nicest people who appear to live for the mission create unimaginable havoc, and you can’t turn a blind eye. Click here for five fraud prevention tips for nonprofit board members.

What does proper segregation of duties look like?

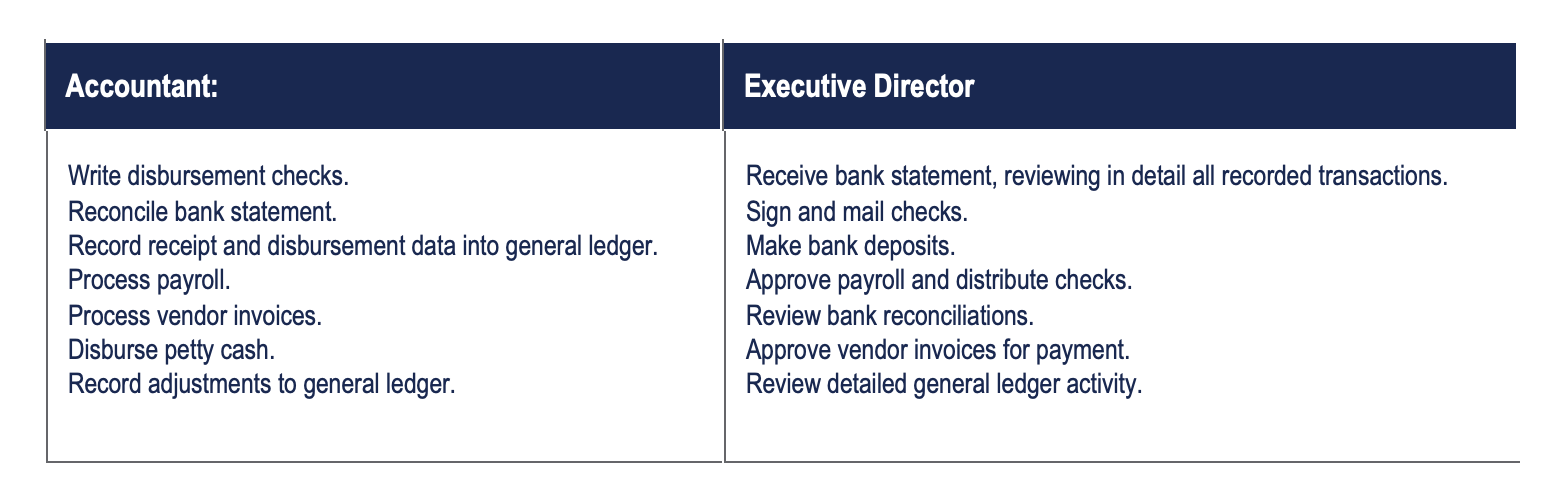

The following is an example of proper segregation of duties when incorporating multiple individuals from across an organization:

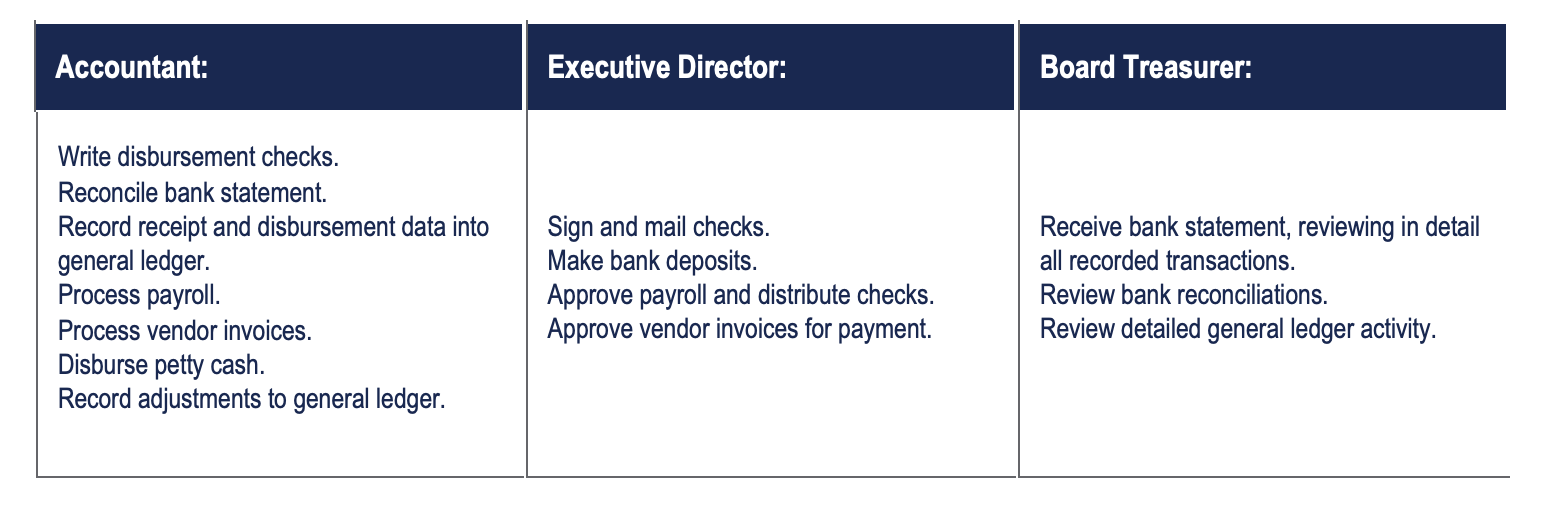

Adding a third person is even better:

As some of the functions mentioned above may be new to an individual, such tasks will require proper training. Within that training, it is important that the individual understands the “why” behind each task.

If there happens to be fraud within an organization and you are part of the governance group, know that there will be at least two side effects. The reputation of the organization will be damaged in the public’s eye, and your personal professional reputation will be damaged.

With that in mind, governance groups need to think of achieving proper segregation of duties and setting up a fraud prevention program as an organizational challenge rather than just an accounting challenge.

How should my organization deal with fraud?

It is important to note that this isn’t a one-and-done implementation. Because job responsibilities change and evolve over time, these processes should be evaluated on a regular basis. As previously mentioned, members of the organization’s governance group should take this as seriously as they do ensuring their personal homes and families are secure while they sleep. And if you do suspect fraudulent activity, forensic data analytics can help identify numerous types of fraud schemes potentially occurring inside an organization.

Identifying and recovering from fraud can be complicated and stressful, but you don’t have to face it alone. Whether you’re looking to ramp up your fraud protection or are reeling from an incident, we can help.